Opening Bell Blitz

Strategy Overview

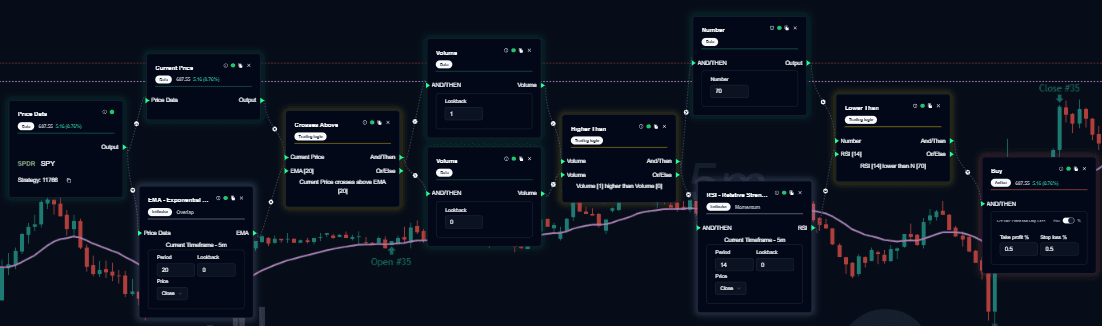

The Opening Bell Blitz framework is a systematic approach to market analysis that prioritizes conviction over simple price movement. It operates on the core principle that price movement without significant volume is often just “market noise” and lacks the fuel to sustain a move.

This strategy ensures that you analyze only setups where market participants are actively “voting” with their capital. By combining price positioning with a volume-based participation filter, it helps identify high-probability structure while avoiding the pitfalls of low-liquidity “fakeouts.”

Indicators & Components Used

| Component | Function |

|---|---|

| Current Price Block | Provides the real-time closing price. This is the “What” of the trade—confirming where the value is currently positioned. |

| Volume Indicator | The “Why” of the trade. It measures the intensity of market activity and validates the strength behind a price move. |

| Volume Moving Average | Establishes a baseline for “Normal” activity. It acts as a benchmark to distinguish between standard trading and a high-conviction surge. |

| Volume Logic (Higher Than) | The primary filter. It requires the current volume to be greater than its average, ensuring only “above-average” interest is considered. |

| Combined Validation | A multi-dimensional gatekeeper that requires price and volume to agree before any analytical signal is output. |

Strategy Logic

Validation Conditions

For an analytical signal to be produced, the market must pass through a strict sequential verification process:

- Participation Surge: The Current Volume must be Higher Than the Volume Moving Average. This confirms that the move is not being driven by a small number of participants.

- Structural Alignment: The Current Price must satisfy a defined positional condition (e.g., holding above a key level or previous candle high).

- Simultaneous Convergence: Both the volume surge and the price position must be valid simultaneously. If price moves but volume stays low, or volume spikes while price stays flat, the strategy remains neutral.

Strategy Behavior & Benefits

- Illiquidity Protection: Naturally stays sidelined during lunch hours, holidays, or pre-market sessions where thin volume can lead to erratic price behavior.

- Deterministic Filtering: Removes the subjective “guesswork” of whether a move “looks strong” by applying a fixed mathematical volume threshold.

- Reduced False Positives: By requiring a dual-layer check, the strategy significantly reduces the number of signals triggered by random price flickers.

- Scalable: The logic is universal and can be applied to any timeframe where reliable volume data is present.

When to Use This Strategy

✅ Best Suited For

- High-Liquidity Instruments: Best performed on Blue-chip Stocks, ETFs (like SPY or QQQ), and major Indices.

- Intraday & Short-Term Analysis: Excellent for validating breakouts in the first 90 minutes of the trading day.

- Continuation Validation: Used to confirm that a pullback is over and the primary trend is resuming with fresh volume.

❌ Not Ideal For

- Thinly Traded Instruments: Assets with “gappy” charts or low daily volume where single orders can distort the data.

- Irregular Volume Sessions: Market environments where volume spikes are erratic and don’t correlate with price movement (e.g., some OTC markets).

- Reliability Gaps: Markets where volume data is delayed or synthesized (some Forex brokers) rather than centralized.

Note: This documentation provides analytical structural recognition and is intended for educational purposes only. It does not constitute financial advice or direct execution instructions.