Volume-Driven Momentum Breakout

Strategy Overview

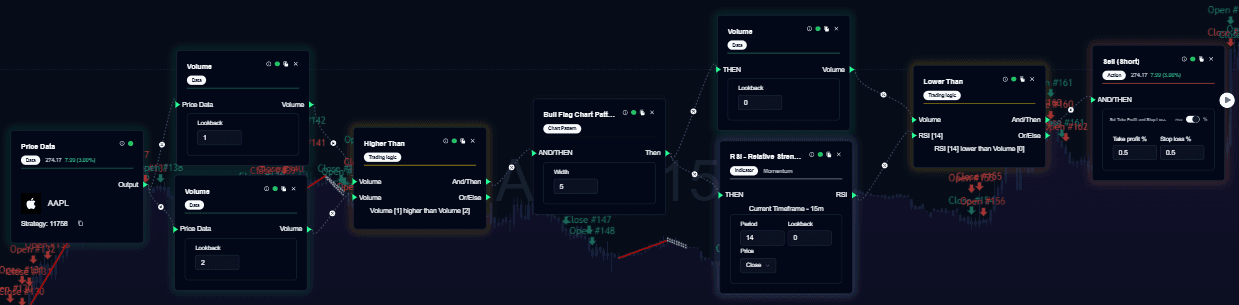

The Volume-Driven Momentum Breakout is a high-conviction system designed to identify and capture moves backed by significant market participation. In trading, volume is often considered the “fuel” of a price move; this strategy ensures that you only enter trades when that fuel is present.

By combining volume surges with price alignment and RSI momentum, the strategy filters out “fake” moves and focuses on high-probability breakouts with confirmed institutional or heavy retail interest.

Indicators Used

| Component | Function |

|---|---|

| Volume | The primary data point. It measures the total number of shares or contracts traded. High volume confirms the validity of a price breakout. |

| Higher Than (Logic) | A comparative block that checks if the current volume is significantly greater than the preceding periods, signaling an abnormal surge in activity. |

| Price Data | Monitors directional movement to ensure price is actually breaking through key levels rather than just spiking and reversing. |

| RSI (14) | Acts as a secondary momentum filter to ensure the move isn’t already exhausted (overextended) before entry. |

Trading Logic

Entry Logic

The strategy follows a strict three-step confirmation sequence to ensure high-quality entries:

- Volume Expansion: The system detects a “Volume Spike” when current activity is higher than the previous average. This suggests institutional involvement.

- Price Alignment: The strategy confirms that the price is closing in the direction of the move (e.g., a green candle for a Buy signal). Volume without price movement is often just churn.

- Momentum Confirmation: The RSI must confirm that the trend has sufficient strength to continue.

Exit Logic

To protect capital and capture the “meat” of the move, the strategy utilizes:

- Targeted Take-Profit: Exiting at predefined structural levels.

- Stop-Loss Protection: Placed below the breakout candle to minimize downside risk.

- Momentum Decay: A secondary exit trigger if volume begins to contract significantly or RSI shows signs of a sharp reversal.

Strategy Behavior

- Activity Dependent: This system is “quiet” during low-volume lunch hours or slow sessions, only triggering when the market is truly active.

- Momentum Focused: It prioritizes trade velocity, typically leading to shorter holding periods than trend-following systems.

- Noise Reduction: By requiring volume confirmation, the strategy avoids the “random walk” of price during low-liquidity periods.

Market Applicability

✅ Best Used In

- High-Liquidity Assets: Large-cap stocks, popular ETFs (like SPY or QQQ), and major crypto pairs.

- Market Opens: The first 60–90 minutes of a trading session, when volume is naturally highest.

- News-Driven Events: Trading the aftermath of earnings or economic data where clear directional volume is present.

❌ Avoid Using In

- Illiquid Markets: Low-volume “penny stocks” where a single small trade can create a false volume spike.

- Holiday Trading: Slow sessions where price action is erratic and lacks real conviction.

- Tight Ranges: Choppy sideways markets where volume spikes may lead to immediate reversals.

Note: This documentation represents analytical structural recognition only and does not constitute financial advice or direct execution instructions.