Volatility Vortex

Strategy Overview

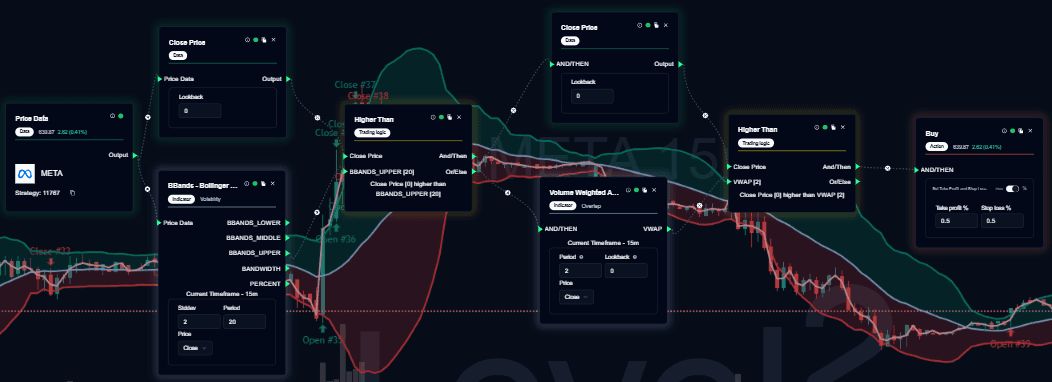

The Volatility Vortex is a systematic validation system designed to ensure that price strength is backed by significant market participation. In professional trading, price movement is often considered deceptive unless it is “validated” by volume.

This strategy focuses on Confirmation over Prediction. It utilizes volume-weighted benchmarks to determine if a move is structurally sound or merely a low-liquidity anomaly. By requiring price to remain above both VWAP and weighted moving averages, the system filters out weak price action and focuses on high-conviction moves.

Indicators & Components Used

| Component | Function |

|---|---|

| Close Price Block | Provides the definitive market value at the end of a period, ensuring analysis is based on finalized data rather than temporary fluctuations. |

| VWAP | The Institutional Benchmark. It represents the average price weighted by volume, showing where the “center of gravity” for the day’s trading lies. |

| VWMA | The Participation Filter. Unlike a standard moving average, the VWMA gives more weight to candles with higher volume, making it more sensitive to meaningful market moves. |

| Price Comparison Logic | A mathematical gatekeeper that evaluates if the current price is holding above these volume-weighted levels. |

| Condition Aggregation | An “AND” logic gate that requires all indicators to be in a bullish state simultaneously before a signal is fired. |

Strategy Logic

Validation Conditions

For the strategy to output an analytical signal, the market must satisfy a strict multi-layered criterion:

- Participation Benchmark: The Closing Price must be Higher Than VWAP. This confirms that the price is trading above the average price at which the majority of the day’s volume occurred.

- Momentum Benchmark: The Closing Price must be Higher Than the VWMA. This ensures that recent price strength is supported by active volume, rather than drifting higher on thin liquidity.

- Simultaneous Alignment: The signal is only valid when both conditions are met at the same time. This prevents “false positives” where the price might be above one benchmark but fails another.

Strategy Behavior & Benefits

- Institutional Alignment: By using VWAP, the strategy naturally aligns its validation with the levels used by large-scale institutional algorithms.

- Noise Reduction: Filters out “low-participation” moves—spikes that happen on low volume, which are prone to immediate reversal.

- Structural Consistency: Ensures that the move has both the position (Price) and the conviction (Volume) before validating the structure.

- Deterministic: Every signal is based on fixed mathematical rules, removing subjective bias and making it ideal for systematic scanning.

When to Use This Strategy

✅ Best Suited For

- Intraday & Short-Term Analysis: Highly effective on 5-minute, 15-minute, and 1-hour charts where volume-weighting is most relevant.

- High-Liquidity Instruments: Best performed on major indices (S&P 500, Nasdaq), Large-Cap Stocks, and high-volume ETFs.

- Trend Validation: Ideal for confirming that a breakout has the necessary “fuel” to sustain a continuation move.

❌ Not Ideal For

- Thinly Traded Instruments: Assets with “gappy” charts or low daily volume where volume data is easily distorted.

- Markets Lacking Volume Data: Some OTC markets or specific Forex brokers provide “tick volume” rather than true volume, which can reduce the accuracy of VWAP and VWMA.

- Irregular Volume Sessions: Avoid during holidays or pre-market/after-hours sessions where participation is naturally skewed.

Note: This documentation provides analytical structural recognition and is intended for educational purposes only. It does not constitute financial advice or direct execution instructions.